Myths and Misconceptions

Setting the Record Straight

As of the end of the fourth quarter of 2021, the Federal Reserve calculated that U.S. public pensions held $5.85 trillion in assets. This staggering collective value alone places a target on pension systems from a myriad of individuals and groups that continue to pursue ways to convert defined benefit pension plans to defined contribution plans. While these efforts have been successful in the private sector, public pension plans have largely avoided this conversion.

Sometimes, these efforts to unravel public pension plans involve the pandering of myths and misconceptions designed to portray defined benefit pensions in an unfavorable way and sway opinions in their favor. When dangerous and misinformed myths and misconceptions surface in the media or in SERS’ own experience, Executive Director Richard Stensrud addresses the topic at a Board meeting and explains why they are false and misleading.

Misconception 1: Investment Managers and Asset Valuations

Misconception: Investments in alternative asset classes, such as private equity, real estate, or private credit, are not transparent, and managers fabricate the return numbers.

Assuring that investment assets are valued correctly starts with due diligence on the fund in which SERS is considering investing. When selecting new investment managers, SERS only considers funds with established track records using proven strategies. System staff thoroughly researches references, confirms there are no sanctions or compliance issues, and looks at the terms of every contract.

SERS also has potential investment funds reviewed by expert investment consultants.

Investment funds are governed by contracts that establish the process, methodology and frequency for valuing assets. If the provisions are insufficient, SERS does not invest in the fund.

Asset values are marked to market and reported to SERS on the cycle set in the contract; depending on the nature of the investment, this can be daily, monthly or quarterly.

Each fund SERS invests in is subject to an annual external audit where the auditors assess and report on whether the asset valuation requirements are being met. Investors receive a copy of the audit report. Many investment funds also have advisory boards that oversee investment funds, including review of asset valuation. SERS frequently serves on such advisory boards and closely reviews the advisory board reports when it does not.

Many investment funds must register with and report to the U.S. Securities and Exchange Commission (SEC). The agency will sanction a fund if there are asset valuation discrepancies.

Internally, SERS has its own valuation committee that reviews valuations received from managers and confirms whether the reports are reasonable or not.

The asset values reported to SERS, and then reported by SERS in its financial reports, as well as the process for establishing those values, are reviewed annually as part of SERS’ independent external audit. If the assets are not fairly valued pursuant to the prescribed process, the auditor will not sign off on SERS’ financial statements.

Together, the valuation requirements and the combination of internal and external oversight, provide strong assurance that assets are valued properly.

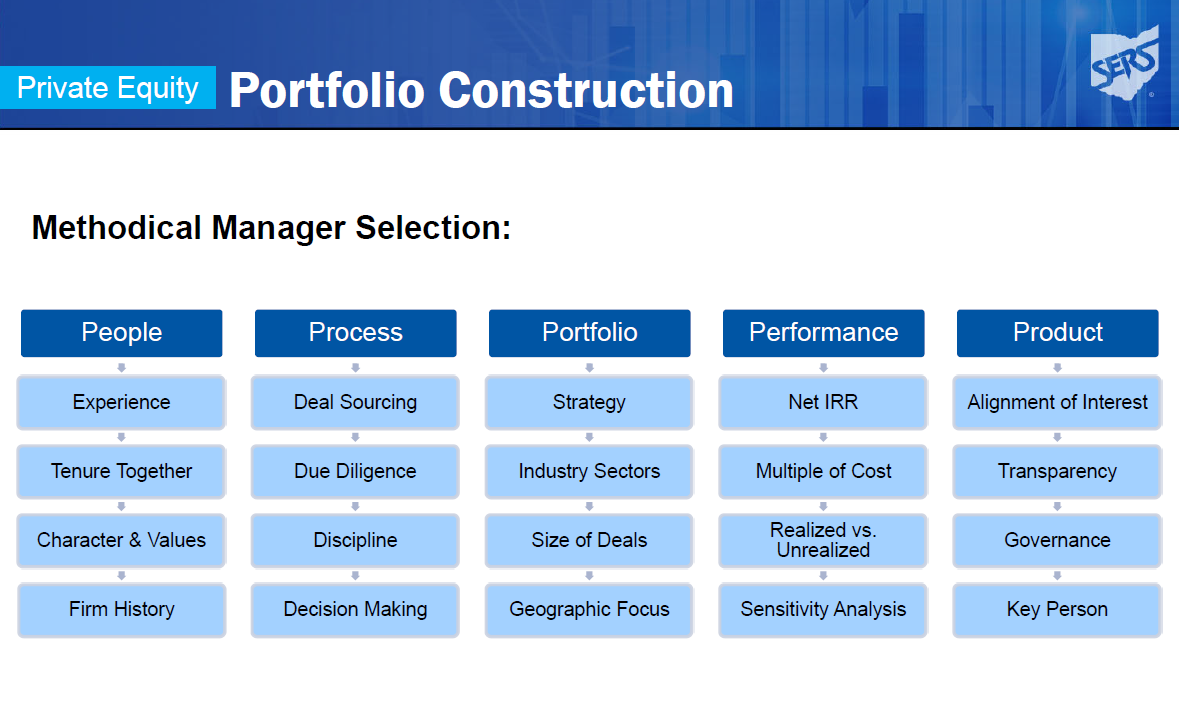

Exhibit A — Numerous reviews staff performs before an investment is approved (from SERS’ October 20, 2022 private equity portfolio review):

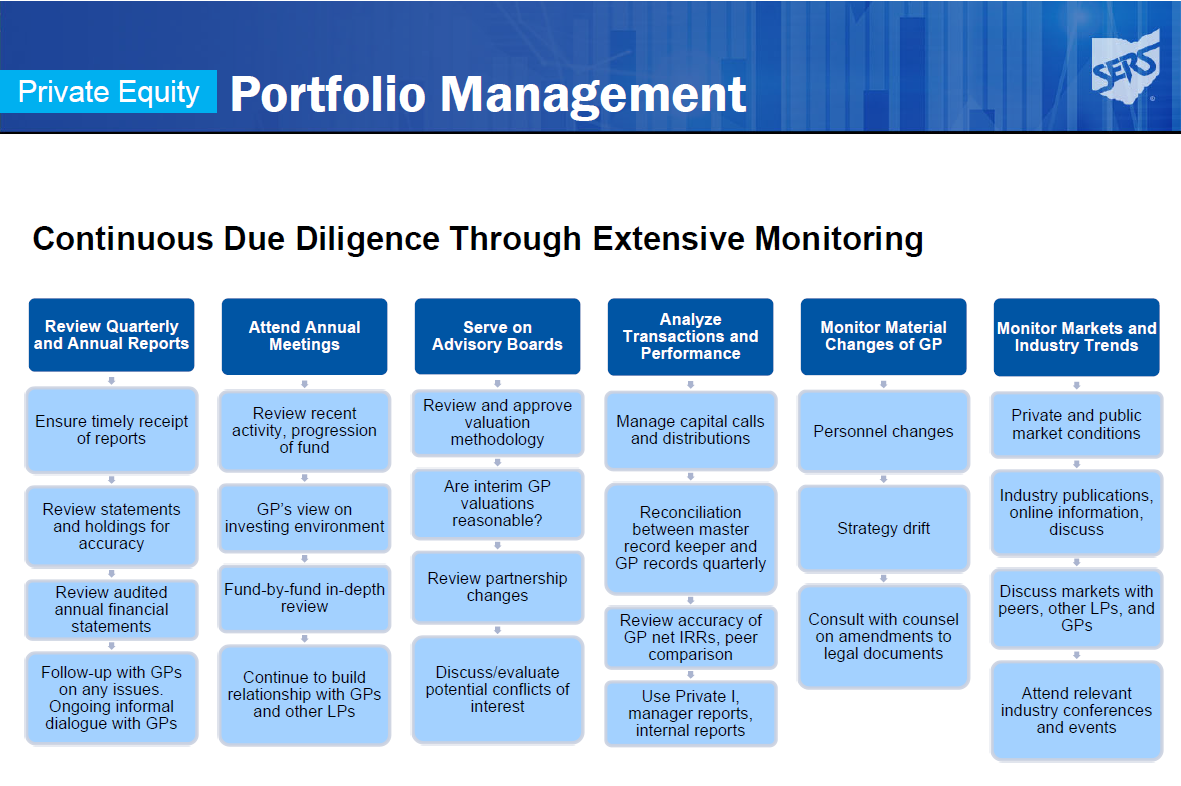

Exhibit B — Asset valuation process and oversight:

Misconception 2: Investment Staff Compensation

Myth: Investment staff incentive pay is too high and that money should be used for benefit payments.

Investment returns are crucial to SERS’ ability to provide pension and health care benefits to current and future retirees. Approximately 70% of the funding for retiree benefits comes from investment returns on the employee and employer contributions received by SERS. Typically, a retiree exhausts their employee contributions and the employer contributions made on the retiree’s behalf in just four to six years of retirement. The remainder is covered by investment returns.

SERS regularly receives independent investment performance calculations from its investment consultant, Wilshire, and biannual reviews from the Ohio Retirement Study Council’s independent investment consultant, RVK.

The most recent calculations from Wilshire for the quarter ended March 2022 indicated SERS’ 1-, 3-, 5-, and 10-year Total Fund returns were all in the top 10% when compared with other U.S. pension system returns. This ranking reflects the strong performance by SERS’ investment team.

To incentivize and reward members of the investment staff for out-performance, SERS has a performance-based compensation plan which provides the investment staff with the ability to earn annual bonuses in addition to their salary. Some important things to note about the performance-based compensation plan:

- The plan is annually reviewed and approved by the SERS Board.

- Whether performance compensation is earned is based on the portfolio’s performance against investment market benchmarks (independent calculations based on the returns of a similar mix of assets) approved by SERS’ Board of Trustees.

- Any compensation earned is not determined by the investment staff themselves. The compensation is calculated by an independent third-party and reviewed by SERS’ Internal Audit Officer, who reports directly to the Board.

Most other large pension systems use a similar mix of salary and bonuses to compensate investment staff for out-performance. The SERS Investment Department Incentive Plan is regularly compared to other U.S. pension system policies to assure that it is consistent with the best and prevailing practices.

Occasionally, performance-based compensation faces misinformed criticism from some members, retirees, media, and other defined benefit pension critics who believe such payouts are excessive. This criticism is often heard when benefit adjustments are needed or investment returns are low.

Even in low-return scenarios, however, investment performance above the benchmark means that significant funding has been added to the pension and health care trusts through the skill and expertise of the investment staff. For example, at a $20 billion pension fund like SERS, for every 1% that performance exceeds the benchmark, the value of the pension trust is $200 million higher. In addition, out-performance in low return scenarios helps position the portfolio for greater returns when economic conditions improve.

Good investment returns are not guaranteed. It takes expertise in assembling and maintaining a diversified portfolio and choosing and overseeing good investment managers. SERS’ Investment Department Incentive Plan fairly rewards the investment team for generating top-tier returns. That investment performance, in turn, substantially enhances the sustainability of the pension and health care trusts, benefiting all SERS members, retirees and employers.

Misconception 3: SERS' Members Retire Young and Receive Lavish Pension Benefits

Misconception: SERS’ members retire young and receive lavish pension benefits.

In the continuing debate over the value of defined benefit pensions, public retirees are sometimes mischaracterized as retiring young and receiving lavish benefits. Not only is this belief untrue, but it unfairly depicts the financial reality of the hardworking people who serve our schools.

SERS’ members are the people who get our children to school safely on buses and keep a watchful eye at busy intersections; they run the business operations and keep track of kids, parents, teachers, delivery personnel, and contractors as they come and go each day; they keep the schools clean and do maintenance that keeps the buildings and buses safe and in operation; they aid teachers in the classrooms and libraries; and they prepare and serve lunches.

They also are the lowest paid of all five Ohio retirement systems.

The numbers make the misconception of SERS members retiring young with lavish benefits clear.

Let’s start with what SERS members earn in their work career:

- 51% of current active SERS members make less than $20,000 annually.

- 83% make less than $40,000 annually.

Next, let’s look at how long SERS members work and how old they are when they retire:

- 75% of service retirees in 2021 had 20 or more years of service.

- 58% of service retirees in 2021 had 25 or more years of service.

- 36% of service retirees in 2021 had 30 or more years of service.

- 58% of service retirees in 2021 were age 65 or older at retirement.

- 89% of all current service retirees are age 65 or older.

Now let’s look at the benefits paid to those retirees:

- 51% of current retirees receive an annual benefit of $12,000 or less.

- 68% of current retirees receive an annual benefit of $18,000 or less.

As a point of reference, the federal poverty level is $12,880 per year.

While a SERS pension is a valuable lifetime benefit, many retirees need additional income from personal savings and/or investments to supplement their pension and retire comfortably. In addition, Ohio is classified as a non-Social Security state, meaning public employees do not pay into Social Security and do not earn qualified service toward Social Security benefits.

Finally, SERS has a large “at-risk” population in that 74% of SERS retirees and 68% of SERS active members are women. Retirement security should not be confused with extravagance. SERS is committed to its mission of providing our membership with valuable lifetime pension benefit programs and services, while helping our membership understand and achieve security in retirement.

Misconception 4: Ohio Public Pensions are Underfunded

Misconception: Ohio public pensions are underfunded, will never be able to pay all the benefits they owe, and the cost to try to do so will crush the taxpayers.

This is untrue on multiple levels.

Ohio’s public pensions are not set up like most other states where funding comes directly from the state budget. Ohio’s pensions are funded by contributions from both employers (school districts, community schools, and some community colleges) and employees. Employers contribute the equivalent of 14% of their SERS employees’ pay and employees contribute 10% of their own wages. Ohio also put contribution rates in statute to prevent increases in taxpayer cost during bad financial times and eliminate the risk of the state missing payments to pension funds. This model has been successful as employer contribution rates have not increased since 1983 and both employer and employee contributions have been made on time and in full.

Pension contributions are not the only source of funding for SERS’ pension benefits. In fact, the largest source of funding — at nearly 70% — are the investment returns earned on the pension trust. This means that nearly 70 cents of every dollar paid in benefits is funded by investment returns.

This combined funding from contributions and investment returns is important for several reasons:

- Pension benefits do not all come due at once, therefore the funding to pay future benefits does not need to be available immediately. There simply needs to be a plan for reaching full funding within a reasonable period of time.

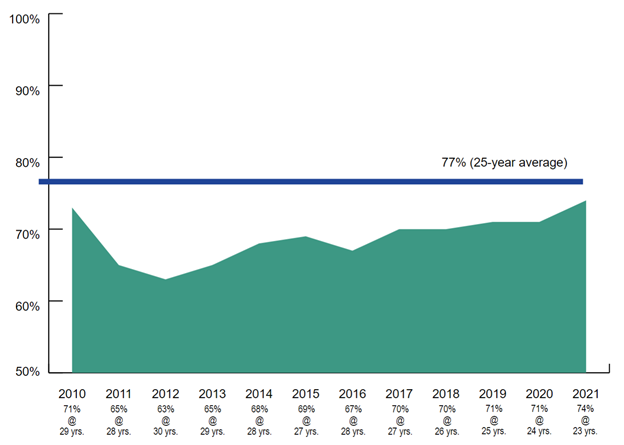

- While SERS’ pension trust is currently 74.46% funded, the stream of future contributions and investment returns will enable SERS to be 100% funded within 23 years.

- Ultimately, nearly 70% of the amount paid to achieve 100% funding will come from investment returns.

Another important factor for assuring the sustainability of the Ohio retirement systems that is somewhat unique to Ohio is the ability to change the benefit structure to reduce the liabilities of the retirement system. Several times over the last 10 years, SERS’ active members and retirees have been asked to make such a sacrifice to help assure the sustainability of the pension fund.

These plan design changes, along with contributions and investment returns, have contributed to a gradual increase in the funded status and a reduction to the amortization period.

In sum, SERS is adequately funded and financially healthy, and SERS’ benefits will be paid as promised, with no increase in the cost to taxpayers.

Misconception 5: A Majority of Public Pension Funds Invest in Cryptocurrencies

Misconception: Public pension funds across the country are putting participants at risk due to investments in cryptocurrencies.

Sometimes you read something that is so wrong you know it’s not an honest mistake. A recent news article titled “Your State Pension is Now Gambling on Cryptocurrency” provides an example.

To support the claim in the title, the author makes the following statement: “…[A]ccording to a recent study, 94% of America’s state and local government pensions – often regarded as the dumbest institutional investors in the world by Wall Street – are gambling on cryptocurrencies.” The claimed source for this statement is a recent “study” by the CFA Institute.

The claim that 94% of public pension funds are investing in cryptocurrencies is so outlandish that the question is how did a reputable organization like the CFA Institute come up with this number? Here’s the answer:

- The CFA Institute conducted a survey, NOT a study. The results of a survey are determined by who responds.

- Of the respondents to the survey, there were 151 US institutional investors. Of those institutional investors, 5% were public pension funds. That means that approximately 7 to 8 public pension funds responded — not exactly a broad representation of institutional investors, and definitely not a true representation of public pension funds.

- It appears that of these 7 to 8 funds, 94% are investing in crypto. That may be why they participated in the survey.

- In no way does this establish that 94% of public pension funds in the US are investing in cryptocurrencies. In fact, the CFA Institute does NOT make that claim. Rather, it is the author who makes that claim.

To be crystal clear: SERS does not invest in cryptocurrencies, and has no plans to invest in cryptocurrencies.

It is troubling that the author sought to stir up fear in hard working public employees by manipulating and mischaracterizing the data to falsely claim that participants in public pension funds across the country are being put at risk due to crypto investments.

Contact Us

We’re glad you’re a member of SERS. If you have questions about your retirement account or benefits, we are here to help.