There are positives and negatives to every plan selection. The highest pension possible, a Plan B “Single Life” plan, provides only for you, the retiree. By choosing a “Joint Life” plan, you can make sure that a benefit will continue to your beneficiary after your death.

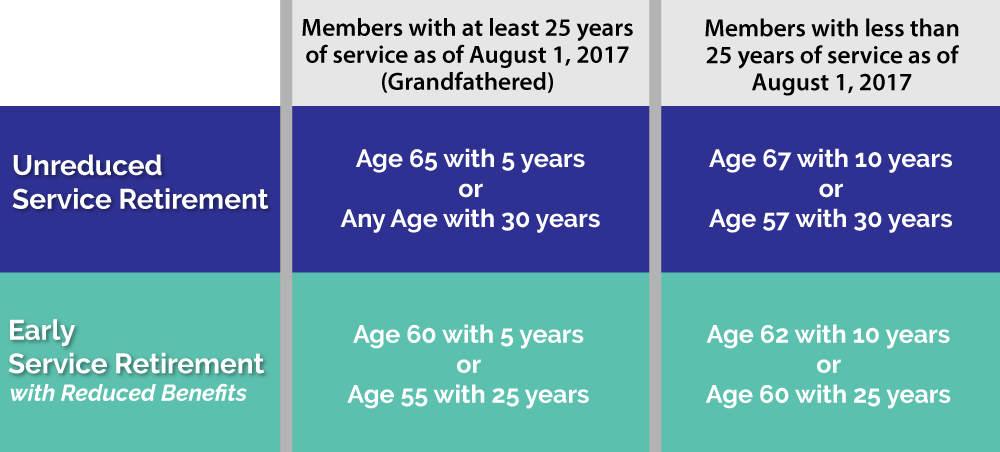

Payment Plans Available

Plan A: Joint Life – One-Half to Spouse

Plan A: Joint Life – One-Half to Spouse

Half of your gross monthly pension is paid to your spouse upon your death. Once your spouse becomes the recipient, payment to your spouse is for his or her lifetime.

Plan B: Single Life Allowance – No Monthly Payment to Beneficiary

Plan B: Single Life Allowance – No Monthly Payment to Beneficiary

This plan pays the highest amount to you, but ceases with your death. If all of your member contributions have not been recovered in the form of monthly benefits, the remainder is paid in a lump sum to your designated beneficiary. If you designate multiple beneficiaries, any amount will be distributed equally among them.

Plan C: Joint Life – Designated Amount to Beneficiary

Plan C: Joint Life – Designated Amount to Beneficiary

You can designate a set percentage or amount for your beneficiary for your beneficiary’s life. This cannot exceed whatever you received; but, if an amount is designated, the minimum must be $100 a month. Federal tax law may require a different minimum amount; in this case, the benefit estimate will show the correct minimum amount allowable.

Plan D: Joint Life – Same Amount to Beneficiary

Plan D: Joint Life – Same Amount to Beneficiary

Plan D provides the same gross monthly amount to your beneficiary that you were drawing at the time of death. Due to federal tax law, if there is too great a difference in the ages between you and your beneficiary other than your spouse, this plan may not be available.

Plan E: Guaranteed Allowance

Plan E: Guaranteed Allowance

You may guarantee beneficiary protection for a limited period of time under Plan E. Several options are available: 5 years, 10 years, 15 years, and other periods are available upon request. The gross monthly amount to your beneficiary is the same amount you were receiving at the time of death. Beneficiary protection is guaranteed for the period of time chosen, and begins with your effective date of retirement. If you designate multiple beneficiaries, the amount payable is the remaining annuity discounted to its present value and will be paid in a one-time lump sum equally among them. If you select this plan, you will be sent a separate form for designation of beneficiaries. This form must be received by SERS before benefits are paid. This plan cannot be changed under any circumstances.

Plan F: Joint Life – Multiple Beneficiaries

Plan F: Joint Life – Multiple Beneficiaries

You may name up to four people to receive monthly benefits upon your death. Each additional beneficiary named reduces your own pension. You must designate a percentage of your monthly pension OR a flat dollar amount for each beneficiary. The amount designated cannot be less than 10% unless required by a court order, and the amount for all beneficiaries cannot exceed 100%. If you are required by a court order to provide a benefit for an ex-spouse, include a copy of the court order. If you select this plan, you will be sent a separate form for designation of beneficiaries. This form must be received by SERS before benefits are paid.